The Stock Market is Going to Crash, Don't Screw Up

The stock market is going to crash, but I’m prepared because the last time I learned the hard way. It was March of 2009, we were in Hawaii and the stock market was on a tear. We had rented a house on the eastern side of Oahu where we could snorkel and kayak from our backyard. And after a year of heavy losses the stock market crash was finally coming to an end. Everything was right in the world, but I was feeling ill – I had just realized my worst financial mistake.

The stock market is going to crash, are you prepared?

Back in 2008, I considered myself a savvy stock investor. I was trading in and out of positions, often using options to further leverage my bets. Much of my spare time was spent reading financial news and tracking stock tickers. Conversations with friends revolved around the hottest stock tips and our next trades. I had been doing this for years, and was making good money. But 2008 was the start of something I hadn’t seen before – the stock market was about to crash.

After an insane run up, the housing bubble burst, shuttering some major banks and bringing others to their knees. Over the course of a year, the S&P500 shed half of its value. Day after day, I watched the financial news, only to hear talking heads spewing doom and gloom. The few wise investors advising to stay the course were drowned out by the mania.

What not to do when the stock market crashes

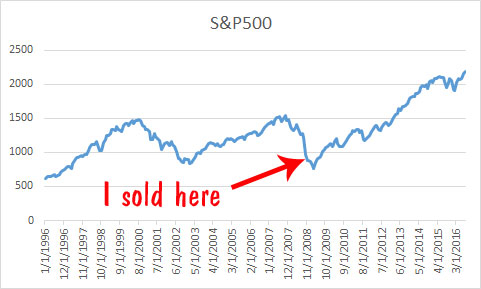

I held on for months, watching my life savings shrink by thousands of dollars each day. Everyone I knew thought the market was going to keep dropping. Finally the pain was too much for me. I traded out of several stock positions, and immediately felt relieved.

The stock market is going to crash, don’t buy high and sell low.

A few weeks later, we went on vacation to Hawaii. In between snorkeling and kayaking, I saw on the news that the market was making a recovery. I was in an awesome place and the market was finally turning around. However instead of euphoria, I felt anguish. It was painful watching all of my stocks sink during the market correction, but seeing that I had locked in my losses by being an idiot was excruciating.

This wasn’t the time to be stressing about financial portfolios.

This wasn’t the time to be stressing about financial portfolios.

I quickly realized my screw-up and started hoping that the stock market would crash again. I wanted a chance to undo my mistake. But there wouldn’t be another dip. This was just the start of a long bull market. I wouldn’t see the prices at which I had sold ever again. This was a painful but important lesson. If you want to sell, you better have a good plan for buying back at a better price. Given the US stock market is always going up, it’s a big risk to get out of the market expecting better prices, especially if the market has already taken a nose dive.

But I like to learn the hard way, and this was an expensive lesson I don’t want to forget. I committed to investing in stocks rather than trading on my instincts. After having missed the first part of the recovery, I plowed my cash back into the stock market. I was lucky to catch the rest of the bull market, and our investments carried us to financial independence allowing us to quit our jobs.

The stock market is going to crash, invest for the long term

These days, I primarily invest in index funds for the long term. I dropped my ego and hung up my trading shoes long ago. It’s saved a lot of time. I no longer spend my days watching financial news, studying quarterly reports, or tracking stock tickers. Being invested for the long term also means there is nothing to burden my mind when on vacations. The losses that I incurred from my mistake are unrecoverable, but I consider them a payment for my education.

Don’t loose your tail when the stock market crashes.

Don’t loose your tail when the stock market crashes.

But seriously, is the stock market going to crash?

As I write this, another bubble is forming, and another stock market crash is approaching. I don’t have to look at the PE 10 or study any financial reports to know it. It’s something I can guarantee because it’s the nature of the market. When this next crash does come, it’s going to be painful, and for new investors it will seem like the apocalypse. Huge amounts of money will disappear in days, and the media isn’t going to coddle anyone.

The stock market is going to crash, but you don’t have to lose out

I learned the hard way, but not everyone has to. The stock market is going to crash, and when it does all hope will be lost. If you despair and sell, you might feel some relief for a while, but the pain you feel when you realize you’ve locked in your losses will be ten times worse. ‘Buy low, sell high’ seems like a basic mantra, but many people will be selling their investments at massive discounts. If you can handle the pain, and overcome the instincts that every cell in your body will want to follow, you can be one of the sharks gobbling up their lunches.